Listen to this blog

Introduction

When loan volumes climb, the pressure on origination teams doesn’t just increase, but it multiplies. Every missed detail, delayed verification, or unclear document request can ripple through the process, slowing closings and putting relationships at risk. In 2025, that’s a risk lenders can’t afford.

Why 2025 is different

The market is already heating up. In March 2025, Reuters reported that Bank of America saw an 80% jump in mortgage applications in the first quarter (Source), well above the typical seasonal rise of around 60%. Lower long-term bond yields and greater housing supply are pushing more buyers into the market. For teams managing mortgage origination, mortgage loan origination pipelines, or loan origination system rollouts, the margin for error is shrinking fast.

In this blog, we’ll explore five things your mortgage origination team can’t afford to overlook in 2025. Addressing these now can protect your timelines, compliance standing, and investor confidence as volumes grow.

Managing sudden spikes in application volume

When lenders are already reporting double-digit jumps in applications early in the year, capacity planning is no longer a quarterly exercise - it should be done on a week-to-week basis. Teams need a plan to scale mortgage origination capacity without compromising review quality.

Tightening pre-fund QC for speed and accuracy

Pre-fund QC is not new, but investor tolerance for defects is lower than ever. In 2025, QC needs to be embedded into the mortgage loan origination process so that issues are caught as files move, not after they’re queued for funding.

Managing documentation from multiple sources

Today, borrowers often submit documents in different formats and through different channels, such as email, portals, even mobile uploads. If these aren’t captured, categorized, and reviewed quickly, it can slow the mortgage origination process. Having a clear intake process and tools that can handle varied document types helps keep files moving without repeated follow-ups.

Preventing automation blind spots

Automation is common, but outdated rules can miss new compliance checks or investor requirements. Regular audits of Loan Origination System (LOS) logic help catch exceptions before they become costly.

Strengthening investor-ready documentation

Investors are scrutinizing mortgage loan origination packages more closely, especially income verifications, asset sourcing, and appraisals. Ensuring the first file submission meets investor standards can protect both timelines and margins.

How Visionet supports mortgage origination teams in 2025

- Flexible document intake and classification

Visionet’s document processing solutions capture, classify, and route documents accurately within the mortgage origination process, irrespective of the channel through which the documentation is submitted - be it email, online portals, or mobile applications. Visionet ensures critical information is readily available and minimizes the risk of delays.

- Built-in quality checks within the process

Visionet’s automation solutions allow lenders to embed checkpoints directly into the mortgage loan origination workflow. This means missing items, inconsistencies, or compliance gaps are identified early, reducing costly rework.

- Data accuracy across systems

Visionet’s integration expertise ensures information flows consistently between the loan origination system and other operational platforms, so underwriters and processors always work with accurate and up-to-date data.

- Scalable operations for peak periods

Seasonal or market-driven spikes in application volume can strain resources. Visionet’s business process outsourcing and technology solutions give lenders the flexibility to scale without sacrificing speed or quality.

- Analytics for proactive decision-making

With Visionet’s data and AI-driven insights, lenders can identify gaps, predict delays, and make informed adjustments, strengthening both efficiency and compliance in mortgage origination.

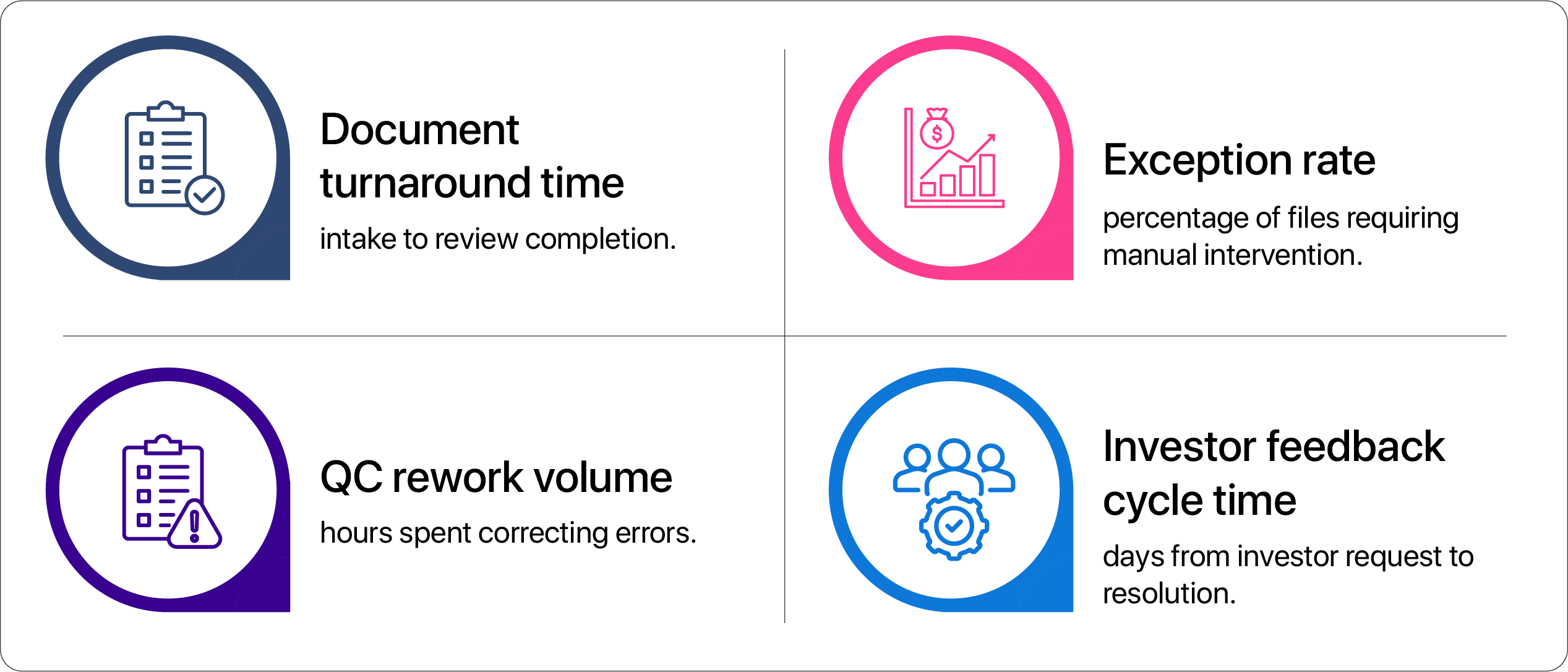

Metrics that matter now

Tracking the right KPIs can guide performance improvements:

Moving from oversight to advantage

In 2025, the lenders who succeed will be those who proactively address operational risks before they escalate, while maintaining speed, accuracy, and compliance even as market conditions shift. Visionet’s proven capabilities in mortgage origination, mortgage loan origination, and loan origination system optimization equip teams to manage higher volumes with confidence and control.

If your goal is to close loans faster without compromising quality, now is the time to align with a partner who can help you get there.

Connect with Visionet to see how our tailored solutions can strengthen your origination process from application to investor delivery.

Ready to move from insight to action?

Whether you’re exploring new opportunities, solving operational challenges, or planning your next stage of growth, Visionet can help you move forward with clarity and confidence.

Speak with our experts to explore how we can support your business goals.