Listen to this blog

Most mortgage leaders measure the borrower experience at the finish line. Post-closing surveys are dispatched, net promoter scores are calculated and contact center logs are reviewed routinely. However, evaluating satisfaction exclusively at the end of the journey provides nothing more than a trailing indicator.

By the time a borrower expresses frustration online or contacts a support desk, the underlying operational breakdown has already been compounding for days. Repeated document requests, protracted silences, and conflicting status updates may manifest as customer service failures, but their roots lie deep within the back-office architecture.

The primary threat to customer retention and satisfaction is not poor front-end communication. It is systemic friction across your mortgage loan processing lifecycle. When disconnected operational teams, poor file visibility, and late-stage exceptions create internal drag, that friction eventually breaks through to the consumer. High-performing lenders understand that anexceptional consumer journey is a direct byproduct of a simplified internal workflow. Forward-thinking institutions eliminate back-office drag to secure the borrower experience long before the consumer ever experiences a delay.

Looking past the trailing metrics of satisfaction

Surveys and feedback loops capture the symptoms of operational distress rather than the root cause. True quality control requires monitoring real-time processing milestones through clean, quantifiable data points.

Service Improvement Cycle:

- Time-to-first-touch: Lenders must measure the exact duration between the initial application submission and the first comprehensive review executed by a processing specialist.

- Silent queue accumulation: Operations teams need to quantify how long a file remains completely stagnant between departmental handoffs, as these operational dead zones directly breed borrower anxiety.

- Exception recurrence rates: Monitoring how often a single file is routed backward for additional verification allows managers to eliminate the systemic errors that trigger late-stage communication loops.

Isolating the operational roots of borrower friction

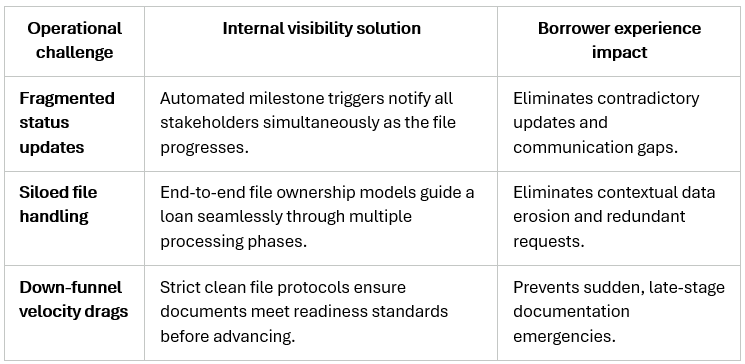

A fragmented back office invariably creates a fragmented consumer journey. Internal operational boundaries almost always mirror external communication breakdowns, directly impacting downstream efficiency.

Contextual data erosion

When a loan file moves across disconnected teams without a centralized tracking mechanism, vital borrower data often vanishes. This internal disconnect forces the consumer to repeat information to multiple institutional representatives, degrading trust.

Distinct data siloes

Mismatched technology platforms cause different operational departments to view conflicting loan statuses. This technical disharmony leads to contradictory updates being delivered to the borrower, damaging corporate credibility.

Delayed exception discovery

Uncovering documentation defects days or weeks into the underwriting cycle results in a sudden, frustrating emergency request for the client. True pipeline efficiency requires identifying these discrepancies immediately at ingestion.

Building absolute internal pipeline visibility

Lenders cannot deliver external clarity to a borrower if the internal team lacks total pipeline visibility. Real-time status tracking must be embedded directly into your core execution model to establish automated milestones.

Turning exception handling into a proactive discipline

Waiting for an underwriting exception to derail a file before reacting guarantees a negative borrower touchpoint. Modern, high-efficiency workflows anticipate complications and isolate them during the initial stages of processing.

This proactive approach requires deploying intelligent data extraction and verification protocols during initial intake to instantly identify documentation gaps. By setting up automated workflows, non-standard files are routed to specialized resolution tracks immediately, preventing complex scenarios from stalling the standard pipeline. Furthermore, instead of trickling requests to the borrower over several weeks, institutions can consolidate multiple underwriting conditions into a single, cohesive outreach.

Aligning the back office with consumer trust

Securing a smooth consumer journey does not require launching detached customer experience initiatives or layering on secondary customer service staff. It requires optimizing your core mortgage loan processing foundation.

This is where Visionet redefines the impact of operational transformation. Through comprehensive enterprise capabilities, the focus shifts away from reactive service intervention and toward the definitive elimination of internal operational friction. By delivering advanced automated document processing and sophisticated intelligent document processing models, Visionet resolves the vulnerabilities that disrupt the lending lifecycle.

By re-engineering file ingestion, establishing granular transparency across production queues, and optimizing interdepartmental handoffs, Visionet helps lenders build a continuous, frictionless fulfillment circuit. When your back-office operation functions with absolute predictability, external responsiveness becomes automatic. The ultimate value of operational simplification extends far beyond standard cost reduction. It directly drives institutional growth, supports comprehensive mortgage life cycle management, and protects your margins.

The borrower may experience the breakdown late, but your operation controls the narrative from the very first step.

Ready to fix your borrower journey from the inside out and eliminate the hidden friction in your pipeline? Discover how our tailored workflows and scalable mortgage processing services can bring total predictability to your operation.

Connect with the Visionet enterprise team today to schedule an executive demonstration.

Ready to move from insight to action?

Whether you’re exploring new opportunities, solving operational challenges, or planning your next stage of growth, Visionet can help you move forward with clarity and confidence.

Speak with our experts to explore how we can support your business goals.