Listen to this blog

Manual condition management is often what slows clear-to-close. As loan files approach the final stage, lenders can lose momentum to repetitive document reviews, validation checks, exception tracking, and stakeholder follow-ups. The result is longer cycle times, higher operational effort, and reduced capacity at the exact moment when speed matters most.

This is the finish line paradox in mortgage operations.

Imagine training for a marathon. You have logged every mile, followed a strict nutrition plan, and sacrificed weekends for months. The finish line is in sight. Spectators are cheering. Then, fifty yards from the tape, you stop to tie your shoelaces. Again. And again. Every single race.

That is exactly what happens inside mortgage lending operations every day. A loan file travels through origination, processing, underwriting, and numerous checkpoints. It consumes weeks of effort. Borrowers are waiting anxiously. Closing dates are circled on calendars. Revenue is close enough to touch. And then, in the final stretch, the file gets caught in a cycle of document reviews, validation checks, and follow ups. What should be a sprint becomes a slow walk.

This challenge becomes even more relevant as market activity begins to recover. Reuters reported a significant rise in mortgage application activity at one of the nation’s largest lenders, reflecting growing momentum across the housing market. As lending volumes begin to increase, many organizations are shifting their attention from demand generation to operational readiness. The question is no longer just how to bring in more business. It is whether existing processes can support greater volume without extending cycle times or increasing costs.

For many lenders, the answer sits inside a process that rarely receives executive attention but directly influences both loan velocity and cost per loan: mortgage condition management.

Source: Reuters, Bank of America mortgage applications jumped 80% in Q1, executive says (March 27, 2025)

Why mortgage condition management becomes difficult to scale

When pipelines are small, mortgage condition management feels manageable. A missing pay stub here. An updated bank statement there. Each review takes only a few minutes.

The challenge emerges when volume begins to grow.

Those few minutes quickly multiply across hundreds of active loans. Teams find themselves reviewing incoming documents, tracking outstanding requirements, coordinating with multiple stakeholders, and ensuring every file stays on course toward clear-to-close.

As volumes increase, several operational challenges begin to emerge:

Challenge | Operational impact |

Growing document volumes | Increased review and validation activity |

Manual tracking processes | Greater risk of missed requirements |

Multiple stakeholders | Slower coordination and follow ups |

Tight closing deadlines | Increased pressure on operations teams |

Individually, these issues may seem manageable. Across an active lending pipeline, they can significantly affect turnaround times and operational efficiency.

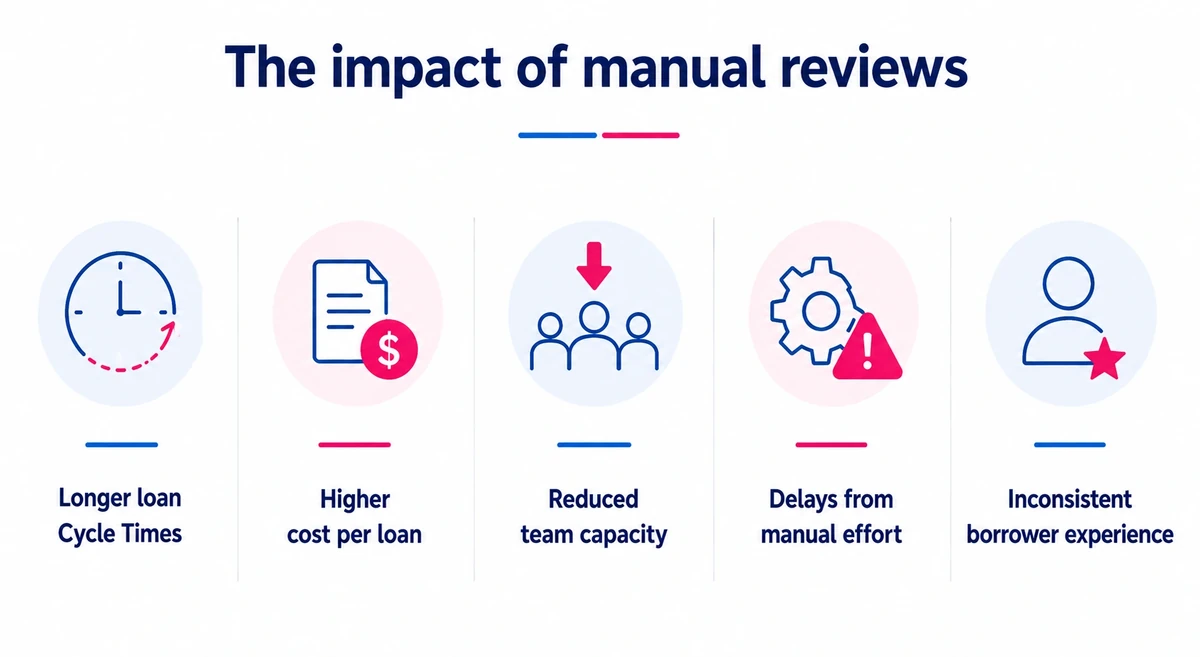

The hidden cost of manual condition reviews

Manual condition reviews rarely create problems on a single loan file.

Their impact becomes visible when viewed across an entire operation.

Every hour spent reviewing routine documentation is time that underwriters and fulfillment teams cannot spend on higher-value work. Every follow up, document check, and validation activity adds incremental effort that can accumulate across hundreds of active loans.

Over time, this can influence key business outcomes:

- Longer clear-to-close timelines

- Higher cost per loan

- Reduced team capacity

- Increased administrative effort

- Inconsistent borrower experiences

As pipelines expand, lenders often face a difficult choice. Add more resources to support growing review volumes or accept slower turnaround times. Neither option is ideal for organizations focused on sustainable growth.

Creating a more focused review process

The conversation around mortgage automation is often framed around speed. In reality, many lenders are pursuing something more valuable: focus.

Not every document requires the same level of human review. Not every file presents the same level of risk. Yet highly skilled professionals often spend valuable time reviewing routine documentation that follows predictable patterns.

Leading lenders are increasingly adopting review models that allow teams to focus their expertise where it creates the greatest impact:

- Routine document validation is handled more efficiently

- Exceptions receive greater attention and oversight

- Underwriters spend more time making decisions

- Fulfillment teams gain better visibility into outstanding requirements

This shift is not about reducing human involvement. It is about ensuring human expertise is applied where it adds the most value.

Clearing the path to close

Visionet helps lenders make that shift. Through intelligent document processing and targeted mortgage processing services, Visionet helps automate the validation of recurring document types while surfacing files that require additional attention. This enables operations teams to spend less time on repetitive document handling and more time on activities that require human expertise and judgment.

The result is a more focused review process, greater visibility into outstanding requirements, and improved capacity to support growing loan volumes without increasing operational complexity at the same pace.

As market activity continues to recover, lenders have an opportunity to reassess the operational processes that influence cycle times, cost per loan, and borrower experience. The organizations best positioned for growth will be those that can scale efficiently while maintaining quality and control throughout the clear-to-close process.

Clear-to-close does not have to be the stage where momentum slows. With the right operating model, it can be the point where efficiency becomes a competitive advantage.

Connect with Visionet to explore how a more efficient approach to condition management can support your mortgage operations goals.

Ready to move from insight to action?

Whether you’re exploring new opportunities, solving operational challenges, or planning your next stage of growth, Visionet can help you move forward with clarity and confidence.

Speak with our experts to explore how we can support your business goals.